The Social Security Decision Worth Six Figures—And How to Keep More From the IRS

You paid into Social Security for decades. At retirement, the system does not send you a personalized playbook—it sends forms. The Social Security Administration’s role is largely administrative: verify eligibility, process claims, and mail checks. Which claiming choice fits your household is a planning question that depends on age, work history, marriage status, longevity, other income, and taxes.

This article walks through individual benefits first, then spousal and survivor rules, then common coordination strategies, and finally how taxes and Medicare premiums interact with your decisions. It is not a recommendation to claim at a particular age. The goal is a clearer map—to help you plan your retirement confidently, and a list of questions worth discussing with a qualified financial and tax professional.

The Social Security system at a glance

More than 68 million people receive benefits from the Social Security system—the #1 federal entitlement program in the U.S., according to the 2025 Trustees Report:

54 million retired workers and dependents

6 million survivor beneficiaries

8 million disabled workers and dependents

Part 1: Individual benefits

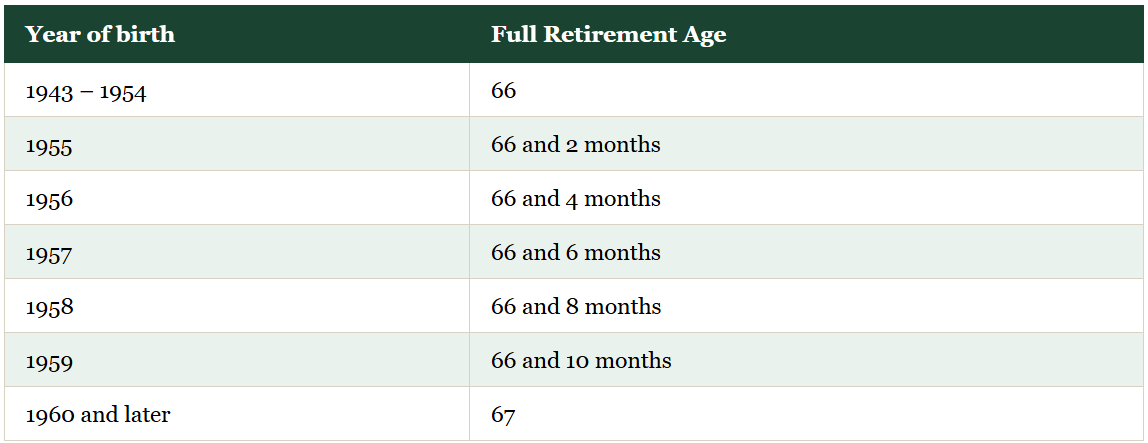

Key terms: PIA and Full Retirement Age (FRA)

Primary Insurance Amount (PIA): The benefit you receive if you wait until Full Retirement Age to collect—your “full” individual benefit before early or delayed adjustments.

Full Retirement Age (FRA): The age at which you can collect 100% of your PIA with no reduction for filing early.

Full retirement age on the year of birth.

Congress has already moved FRA upward once; treat any future increase as uncertainty, not a forecast.

How retirement benefits are calculated

You will never need to run this math yourself—it is on your my Social Security statement. The steps explain why nearly everyone has a different benefit:

Step 1 — Index the earnings record. SSA uses reported earnings (up to ~40 years on your wage statement). At age 60, each year’s earnings are adjusted for wage inflation.

Step 2 — Average Indexed Monthly Earnings (AIME). SSA totals your highest 35 years of indexed earnings and divides by 420 months. If you have fewer than 35 years of covered work, zero years still count in the divisor—often lowering the benefit versus your actual working-year average.

Step 3 — Calculate PIA using a progressive formula. For workers first eligible in 2026, bend points apply roughly as follows (amounts update annually):

90% of the first $1,286 of AIME, plus

32% of AIME from $1,286 through $7,749, plus

15% of AIME above $7,749

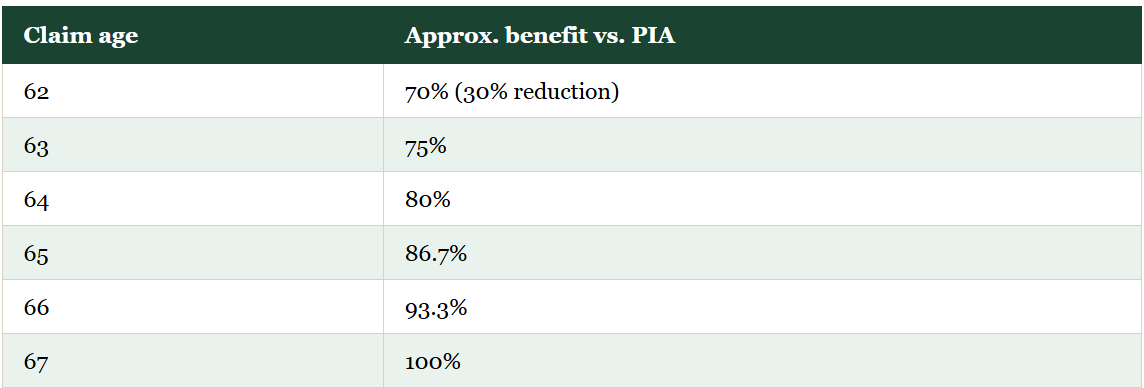

What if you claim benefits early?

Individual retirement benefits can start as early as 62, but reductions are permanent (with limited repair options—see Part 3). For someone whose FRA is 67:

Approximate benefits vs. PIA at different claim ages.

SSA data show about 50% of men and 52% of women take reduced benefits at 62—often without modeling spousal, survivor, tax, or Medicare effects.

What if you delay past Full Retirement Age?

For each month you wait beyond FRA (up to age 70), benefits grow about 2/3 of 1% per month—roughly 8% per year. Waiting until 70 yields about 124% of PIA when FRA is 67. There is no additional credit for delaying past 70.

If someone claims at 68½, they are not giving up a full year’s 8% bump by missing their 69th birthday—they earn credit month by month.

When to commence benefits: early, FRA, or age 70?

Everyone has the same three levers: early, FRA, and delayed credits. Here is an illustrative example: PIA = $2,000, FRA 67 (not adjusted for COLA):

An example for approximate monthly benefit at different claim ages.

That is a 77% spread between the age-62 and age-70 monthly checks. What are the differences in cumulative lifetime income?

Breakeven points

Breakeven compares lifetime benefits, not the first check alone. Using the $2,000 PIA example, assuming 3% annual COLA and death at 95:

Monthly benefits and illustrative lifetime benefits at different claim ages.

Approximate breakeven ages (same assumptions):

Socail security benefit breakeven ages. For example, if you live beyond age 76, your lifetime Social Security benefits will generally be higher if you begin claiming at age 67 rather than at age 62. (Only for illustration)

Even if you do not expect to live to 95, delaying can still win on lifetime income if you pass these breakeven ages—and the longer you live past them, the larger the advantage.

Longevity: the hardest variable

The longer you live, the more valuable delaying tends to become. For a 65-year-old couple today, actuarial tables often cite roughly a 50% chance that at least one spouse lives to 93 and a 25% chance past 98.

For couples, the question is not always “Will we both live a long time?” but “What if one of us lives a long time?” Survivor benefits—covered in Part 2 and Part 3—often drive the answer.

But none of us ever knows when life’s journey will come to an end. This morning, I learned that one of our well-known alumni passed away from cancer. He was only 55 years old. It was a sobering reminder of how precious and unpredictable life is.

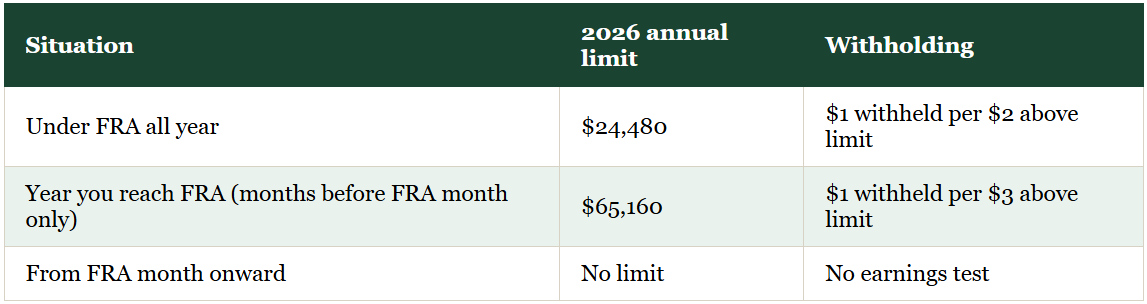

Working while collecting Social Security

If you collect benefits before FRA and keep working, the retirement earnings test may temporarily withhold part of your check.

What counts: Earned income only—wages and net earnings from self-employment.

What does not count: Passive income—pensions, dividends, interest, capital gains, rental income, and IRA withdrawals.

2026 limits (SSA COLA fact sheet):

2026 annual income limit for retiment earnings test.

SSA does not keep withheld benefits permanently. At FRA, withheld amounts are credited back and your benefit is recalculated upward. The test is partly asking: do you need the benefit check if you are still earning substantial wages?

Example — John, age 62

Annual benefit (already reduced for early claiming): $12,000

Still working; earns $32,000

$7,520 over the $24,480 threshold → SSA withholds $3,760

John receives $8,240 that year instead of $12,000

At FRA (67), the earnings test ends, credits apply, and his benefit recalculates

Part 2: Spousal and survivor benefits

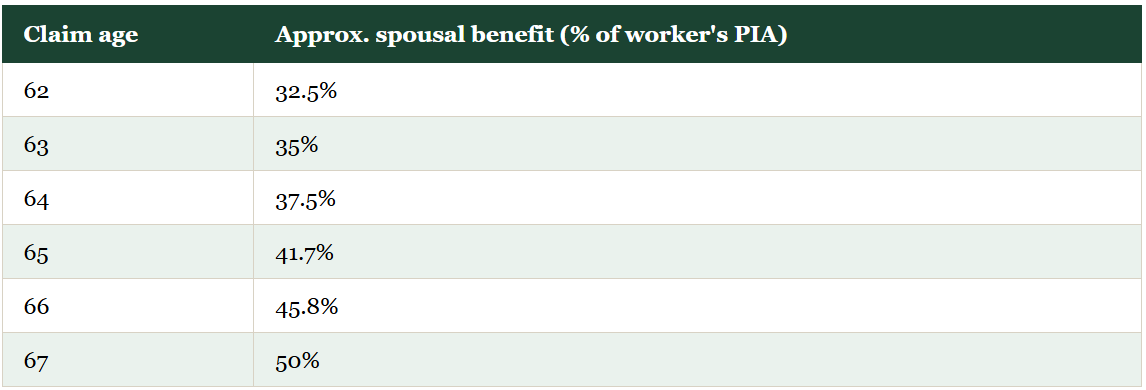

Five rules for spousal benefits

To collect on a spouse’s record, the worker spouse generally must be receiving benefits (ex-spouse rules differ—see Part 3).

Spousal benefits are based on 50% of the worker’s PIA—not 50% of what the worker actually receives if they claimed early.

Spousal benefits can start as early as 62, with reductions if taken before the spouse’s FRA.

Spousal benefits do not grow after FRA. There is no benefit to delaying spousal benefits past FRA.

If you qualify for both your own benefit and a spousal benefit, you receive the higher of the two—not both added together.

How spousal benefits are calculated (Gary and Amy)

Gary’s FRA benefit (PIA) is $2,000. Amy’s own FRA benefit is $500. At her FRA, Amy is entitled to the greater of:

50% of Gary’s PIA: $1,000, or

Amy’s own benefit: $500

Amy’s benefit is $1,000 (the spousal amount). She does not collect $500 + $1,000.

Even if Amy never worked or lacks 40 credits, she may qualify on Gary’s record—but Gary must file for Amy to claim spousal benefits on his record.

Taking spousal benefits before Full Retirement Age

If the lower-earning spouse files before FRA 67, both the own benefit and any spousal component can be reduced:

Taking spousal benefits before Full Retirement Age.

Six rules for survivor benefits

Generally must have been married at least nine months (exception for accidental death).

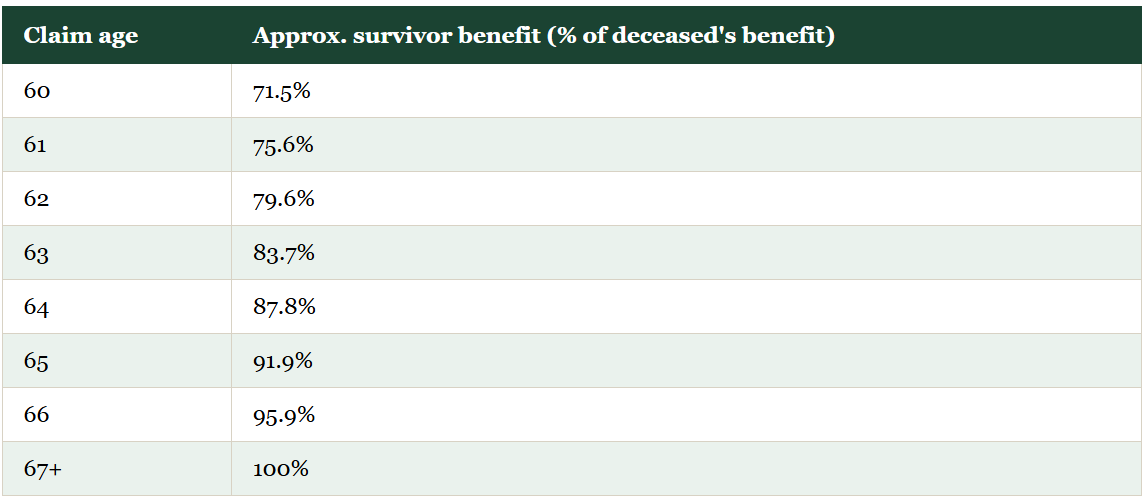

Survivor benefits can start as early as 60, with reductions up to about 28.5% if taken before FRA.

At FRA, survivor benefits equal 100% of the deceased spouse’s benefit (what they were receiving or entitled to receive).

Minor children may qualify if under 18 (or up to 19 if still in high school).

Widows/widowers with children under 16 may qualify regardless of age.

The earnings test applies to survivor benefits as well.

When one spouse dies, one check stops. The survivor receives the higher of their own benefit or the deceased’s benefit—you cannot keep both. A survivor can switch between own and survivor benefits over time, but only one at a time.

Important: Unlike your own retirement benefit, survivor benefits do not increase after FRA. If survivor benefits are available, there is generally no reason to delay past FRA—that is the maximum.

Taking survivor benefits before Full Retirement Age.

Part 3: Common maximization strategies

Couple example: Gary and Amy (both 62, FRA 67)

Gary’s FRA benefit: $2,000

Amy’s FRA benefit: $500

Amy’s FRA spousal benefit: $1,000 (Gary’s spousal amount would be $250—not relevant here)

Strategy 1 — Both collect at Full Retirement Age

Gary collects $2,000 at FRA.

Amy collects $1,000 spousal at FRA (she may never need her own $500 record).

At Gary’s death, Amy increases to ~$2,000 survivor benefit.

Strategy 2 — Higher earner delays; lower earner starts at FRA

Amy collects her own $500 at FRA, then increases to $1,000 spousal.

Gary delays to 70 and collects $2,480.

At Gary’s death, Amy increases to ~$2,480 survivor benefit.

Provides income from Amy’s record ages 67–70 while Gary’s benefit grows.

Strategy 3 — Lower earner takes early; higher earner delays

Amy collects her own ~$350 at 62; spousal portion rises to about ~$850 (both reduced for early filing).

Gary delays to 70 and collects $2,480.

At Gary’s death, Amy’s survivor benefit is ~$2,480 if she switches at FRA or later—her early own benefit does not permanently reduce a full survivor benefit taken at FRA+.

Strategy 4 — Both take early

Gary collects $1,400 at 62.

Amy collects ~$700 spousal at 62.

At Gary’s death (illustration: age 80), Amy’s survivor benefit may be only ~$1,400—because Gary’s reduced benefit permanently caps the survivor amount.

If the higher earner claims early, survivor benefits are permanently reduced too.

Widow example: Wendy (age 60)

Wendy’s spouse died at 67 while receiving $2,400/month (his FRA benefit). Wendy’s FRA is 67.

Wendy's own benefit and survivor benefit at different ages.

Survivor benefits do not grow past FRA—$2,400 at 67 is the same at 70.

Strategy 1 — Survivor benefit at 60

Receive $1,716/month from age 60.

Can switch to her own benefit later by filing—if she does not, she stays on survivor.

Strategy 2 — Own benefit at 62, switch to survivor at FRA

Receive $1,400/month from 62.

At 67, switch to full $2,400 survivor benefit.

Taking her own benefit early did not prevent a full survivor benefit at FRA.

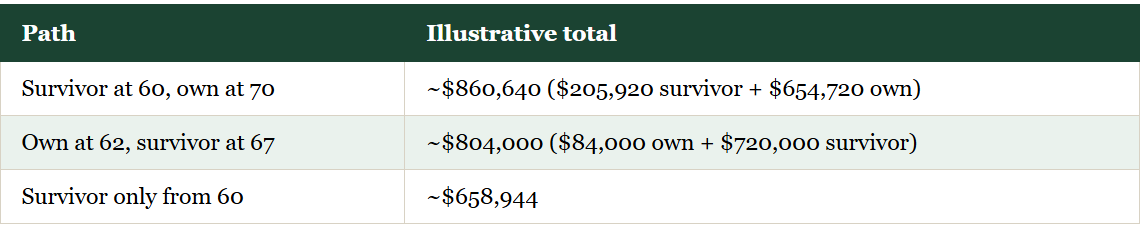

Strategy 3 — Survivor at 60, switch to own at 70

Receive $1,716/month from 60.

At 70, switch to $2,480 own benefit (maximized with delayed credits).

Early survivor benefits did not block her own benefit later.

Works best when own benefit at 70 exceeds the survivor amount.

Illustrative lifetime totals to age 92 (example only; not a forecast):

Survivor at 60 and swith to own at 70 works best in this example.

Divorced spouses

Living ex-spouse — you may qualify if:

Marriage lasted at least 10 years

You are currently unmarried

You are at least 62

Your ex is entitled to benefits

Unlike current spouses, your ex does not have to file for you to claim divorced-spouse benefits.

Deceased ex-spouse — survivor benefits may be available from age 60 if the marriage lasted 10+ years and you did not remarry before 60.

Part 4: Taxation of Social Security and Medicare

Federal taxation: provisional income

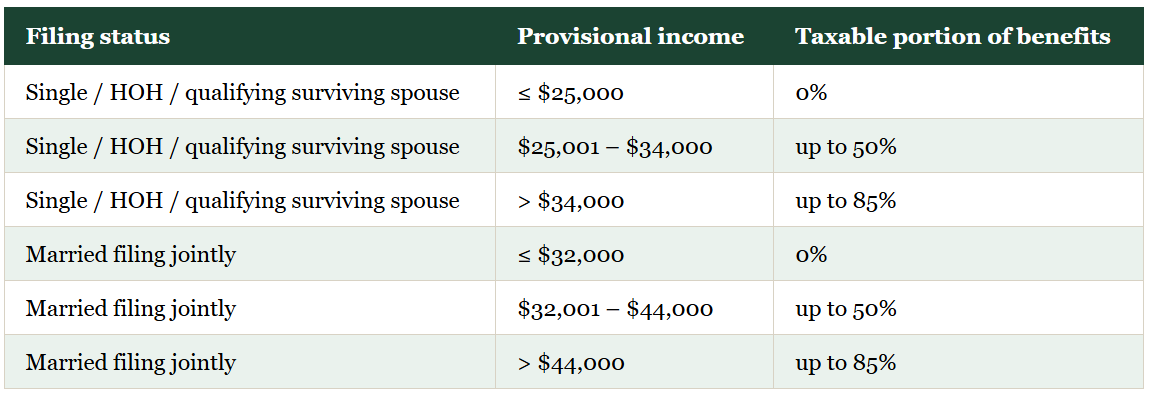

Up to 85% of Social Security may be included in federal taxable income—never 100%. The IRS uses provisional income (also called combined income):

Provisional income ≈ Adjusted gross income (excluding SS) + tax-exempt interest + 50% of Social Security benefits

These thresholds were set in 1983 and 1993 and are not indexed for inflation—so more middle-income retirees pay tax on benefits over time.

Provisional income threshold and social security tax.

Included in provisional income: half of Social Security, municipal bond interest, wages, business income, interest, dividends, capital gains, traditional IRA distributions, rental income.

Generally excluded: tax-deferred growth inside IRAs/401(k)s/annuities; qualified Roth IRA and HSA withdrawals; non-taxable life insurance proceeds.

Senior standard deduction (2025–2028)

Federal legislation added an extra $6,000 standard deduction for taxpayers 65+ ($12,000 MFJ if both qualify), scheduled to sunset after 2028. Phase-out ranges: $75,000–$175,000 (single) and $150,000–$250,000 (MFJ). Applies whether you take Social Security or itemize—confirm current law with your tax preparer.

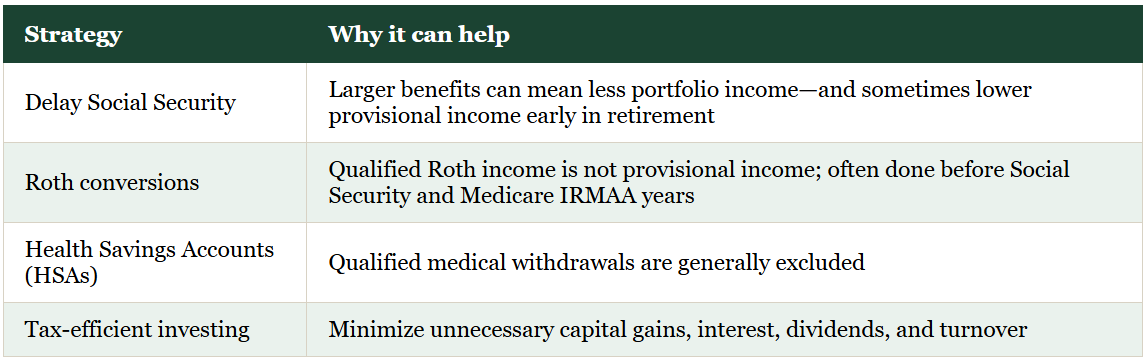

Strategies of managing provisional income.

Medicare and Social Security

If you receive Social Security at 65, you are typically enrolled automatically in Medicare A; Part B premiums are usually deducted from your benefit.

If you are not collecting Social Security at 65, you may need to enroll actively (unless employer coverage applies) and pay Part B out of pocket.

IRMAA (Medicare income surcharges)

IRMAA adds surcharges to Part B and Part D when modified adjusted gross income exceeds thresholds based on your tax return from two years prior. For 2026 premiums, SSA generally uses 2024 MAGI.

2026 Part B standard premium: $202.90/month

IRMAA begins above $109,000 (single) or $218,000 (joint)

Premiums rise through several brackets up to $689.90/month at the highest tier

Large one-time events—Roth conversions, capital gains, RMDs—can trigger surcharges two years later. Life-changing events may allow a reduction request via Form SSA-44.

As a financial advisor, I’ve seen many clients overlook the impact of IRMAA when planning Roth conversions. As a result, they inadvertently trigger higher Medicare Part B premiums that could have been avoided with proper planning.

Retirement income planning: where Social Security fits

Social Security is on average about one-third of retirement income for many households.

Traditional employer pensions have shrunk: private defined-benefit plans peaked around 175,000 in 1983 and fell to about 46,500 by 2022 (U.S. Department of Labor). Personal savings and claiming strategy matter more than for prior generations.

Match income to expenses:

Retirement income planning: match income to expenses.

The goal many planners use: cover essentials with income you cannot outlive; fund discretionary spending from sources where you can adjust in down years.

Summary

Social Security is a critical part of retirement income—but rarely the only part.

Claiming age, spousal coordination, and survivor protection can change lifetime results by six figures in illustrative examples.

Taxes, provisional income, and IRMAA belong in the same conversation as benefit quotes.

There is no one-size-fits-all best age—only what fits your cash flow, longevity, and tax picture.

Action checklist

Know your benefits — download your Social Security statement.

Calculate retirement expenses and income — essentials vs. discretionary.

Compare claiming strategies — individual, spousal, and survivor paths.

Model taxes and IRMAA thresholds — not just gross Social Security.

Book a consultation — review your situation comprehensively (cash flow, tax, risk, investments, estate).

Disclaimer

This article is for informational and educational purposes only and does not constitute tax, legal, or individualized investment advice. Social Security rules, tax law, and Medicare premiums change. Confirm current figures on ssa.gov and irs.gov before making decisions.