Retirement Income Strategies: Without a Single “Magic” Investment

When you leave a steady paycheck, your portfolio has a new job: turn accumulated wealth into reliable spendable income—often for decades—while leaving room for growth, legacy, and tax efficiency. There is no single investment that solves every problem. What usually works is matching money to time horizons and spending jobs.

This article walks through two frameworks we use constantly:

1. Three buckets by time horizon — short-term liquidity, mid-term planned spending, and long-term retirement/legacy funding.

2. An income pyramid for long-term spending — separating fixed essentials, variable lifestyle, and legacy/growth.

Together they answer the same underlying question: Which dollars need certainty, which can tolerate risk, and when do you need access?

Why these two frameworks matter (especially without a paycheck)

While you were working, a market dip could be uncomfortable—but human capital (future earnings) often acted as a backstop. In retirement, many households cannot earn their way back from losses on the dollars they spend every month.

That does not mean hiding everything in cash. It means building enough certainty where certainty matters, so the rest of the plan can still pursue growth and flexibility.

These frameworks work for many retirees because they are behavioral as well as technical: they reduce the odds you sell long-term investments at the worst moment to cover near-term shocks—or confuse an IRS distribution rule with a sustainable lifestyle budget.

Framework 1: Three buckets

Think of your assets as sitting in three time horizons. The labels are simple; the discipline and rebalancing are what makes them work.

Bucket 1 — Short term: emergency reserve

An emergency fund is not optional storytelling—it is liquidity for life. Healthcare surprises, family emergencies, home repairs, or other costs rarely arrive on schedule.

Why it matters: Without it, people often raid investments meant for five or fifteen years away, or tap credit at high rates. That breaks the rest of the plan.

How to build it: Through steady discipline—automatic transfers, bonus allocations, or intentional trims until you reach a target your household agrees on. As a practical planning band, many retirees anchor emergency liquidity around three to twelve months of essential expenses. The right endpoint depends on pensions, premiums, deductibles, dual incomes ending, and plain sleep-at-night preference.

Where we typically park it:Money market funds or high-yield savings—places meant for stability and same-week access, not maximum long-run return.

Bucket 2 — Mid term: known expenses in the next few years

This bucket is for money you expect to deploy—but not tomorrow and not purely for thirty-year retirement cash flow. Examples:

Replacing a vehicle

A planned gift or family support

Setting aside dollars for Roth conversions (taxes due on converted amounts, learn more: Roth Conversion Gap Years Strategy: Avoid IRMAA & Capital Gains Tax | 2026 Guide )

Where timelines and suitability align, we commonly allocate mid-term funding across tools such as structured notes, multi-year guaranteed annuities (MYGAs) or similar fixed-period contracts, and balanced / conservative portfolios that dial equity risk below what we would use for multi-decade legacy money.

Investment posture: Generally moderate risk at most. The theme is simple: do not treat next-three-years money like thirty-years money—and do not fund known near-term liabilities purely from volatile sleeves unless you consciously accept selling into downturns.

Bucket 3 — Long term: retirement lifestyle and legacy

This bucket funds spending across retirement—and connects directly to the income pyramid below. Long-term dollars can pursue growth only because buckets one and two reduce forced selling during storms.

Framework 2: Income pyramid (how long-term spending breaks down)

Once you are inside long-term retirement funding, not all expenses behave the same way. We often picture three layers:

Layer A — Fixed expenses (the foundation)

These are costs you cannot easily dial down without major lifestyle change: housing, utilities, insurance premiums, baseline groceries, medications not covered elsewhere, and similar recurring essentials.

Common funding sources:

Social Security

Pensions

Federal retirement income for annuitants

If guaranteed income does not fully cover this foundation, households sometimes consider:

Income annuities (immediate or deferred—trade liquidity for predictable cash flow), and/or

Disciplined withdrawals from a diversified portfolio, anchored by withdrawal-rate research (often discussed as the “4% rule”—more below).

The goal is predictability on the floor, not maximizing the long-term return. (Learn more: Spending Through the 3 Stages of Retirement (Go-Go, Slow-Go, No-Go) — and What It Means for Your Plan)

Layer B — Variable expenses (flexible lifestyle)

This layer covers spending you could trim in a bad market year: travel, hobbies, generous gifting beyond essentials, long-term care services, upgrading vehicles ahead of schedule, and similar discretionary choices.

Common funding approaches:

Dividend-oriented equity

Registered index-linked annuities (learn more: RILA: Registered Index-Linked Annuities Explained | Buffers, Caps, Hidden Costs)

Diversified portfolio

Income-oriented structured notes

Private credit/private infrastructure, or other alternative income exposures—often illiquid, higher minimums, and not appropriate for everyone

Insurance

Variable expenses belong here because they pair better with volatile sources: when distributions dip or markets stumble, you can adjust lifestyle without jeopardizing the foundation.

Layer C — Legacy and long-term growth

If you have assets beyond lifetime lifestyle needs—or clear charitable intent—this layer can prioritize maximum expected growth over long horizons, tax-efficient transfer, and simpler stewardship for heirs based on the risk tolerance.

Holdings we explicitly discuss with clients:

Growth-oriented portfolios: Broad equity exposure tilted toward long-term capital appreciation rather than current yield—often implemented through diversified funds or separately managed equity strategies, depending on account type and preferences.

Concentrated or thematic sleeves: Some families intentionally maintain concentrated equity (like tech-heavy portfolio) intended for children or charity, accepting deeper drawdowns because no one is paying the electric bill from that sleeve.

Tax and transfer mechanics: Beneficiary designations, trusts where appropriate, Roth strategies, stepped-up basis considerations for taxable holdings, and insurance only where it fits—legacy is partly portfolio construction and partly documentation.

Volatility here may be acceptable precisely because it is not earmarked for next month’s groceries. Concentration still deserves honest conversation: heirs inherit both upside and downside—so sizing and communication matter as much as ticker selection.

Withdrawal rates: what “4%” actually means (and why your withdrawal rate moves)

The popular “4% rule” label comes from historical research on safe withdrawal rates. In the classic framing:

You choose an initial withdrawal as a percentage of the portfolio at retirement (often cited around 4%, though Bengen’s original worst-case figure under stated assumptions was 4.15%).

After that first year, you'd forget the 4.15% and simply give yourself a cost-of-living-adjustment (COLA) based on the prior year's inflation (CPI, or Consumer Price Index)—rather than mechanically withdrawing “4% of whatever the portfolio is worth today” every single year.

For example, if you had a portfolio worth $100,000, you'd withdraw $4,150. Next year, your withdrawal will be $4,274.5 based on a 3% inflation. In that sense, your withdrawal scheme functioned much like Social Security does today.

That distinction matters: many misunderstandings come from treating it like a perpetual “four percent of balance” formula.

What it is not.

Not a promise you will maximize ending wealth—many paths leave large leftovers by design, because the academic exercise emphasized surviving poor sequences.

Not a universal recommendation—your horizon may not be thirty years; your mix may differ; taxes and fees change outcomes.

William Bengen’s work is widely associated with the “4% rule,” targeting roughly a 30-year horizon using U.S. historical data in the original framing. In later commentary and his 2025 book A Richer Retirement, he discusses updated mixes and figures around ~4.7% under revised assumptions—assumptions matter. See Bengen’s discussion.

No single strategy fits everyone

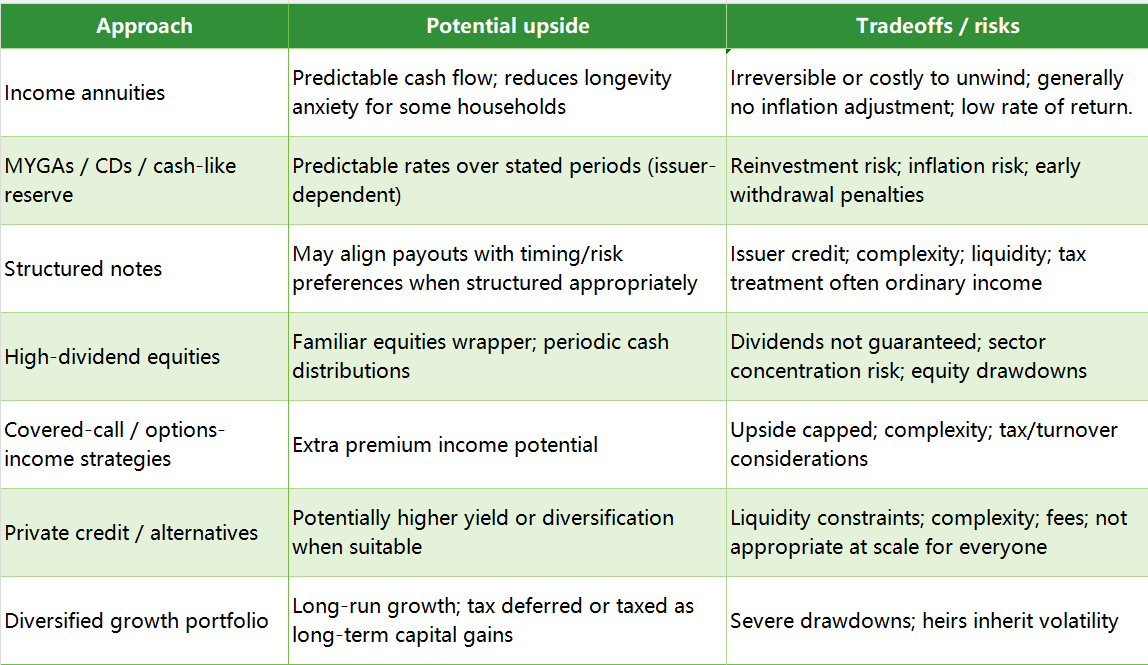

Every tool solves something—and breaks something else. Tax bracket, liquidity needs, risk tolerance, state rules, and contract fine print matter more than slogans.

The pros and cons of different investment approaches.

Retirement income planning is less about finding one perfect product and more about matching investments to jobs: certainty where paychecks used to hide shocks, moderation for mid-term goals, and—inside long-term funding—a pyramid that separates fixed essentials, flexible lifestyle, and legacy.

Disclaimer: This article is educational and not individualized advice. Structured products, annuities, private investments, real estate programs, and withdrawal strategies involve costs, risks, and tax consequences that depend on your situation. Consult qualified tax and legal professionals before transactions. Investing involves risk, including possible loss of principal. Past performance does not guarantee future results.