Turning 65? A Smarter Medicare Game Plan

If you are about 64 and planning to retire, Medicare is probably on your mind—and it should be. You do not have to become an expert overnight, but you do need a clear picture of how Parts A and B work, how premiums interact with Social Security, and why your last few working years on your tax return can still affect what you pay in retirement.

Why Your “Medicare year” Starts Before Age 65?

For most people, Medicare eligibility begins at age 65. Your Initial Enrollment Period generally runs seven months: the three months before the month you turn 65, the month of your birthday, and the three months after. Miss the right window without other creditable coverage, and you can face lifetime late-enrollment penalties on Part B (and sometimes Part D).

If you still have employer coverage, the rules change—especially the 20-employee threshold. With 20 or more employees, your group plan is usually primary; you may be able to delay Part B without penalty while that coverage is in force. With fewer than 20 employees, Medicare is often primary, which means you generally should enroll when first eligible or risk denied claims. Confirm with your HR team in writing.

Part A (hospital) is premium-free for most people who paid Medicare taxes long enough. Many sign up for Part A at 65 even if they keep working—unless you want to keep funding an HSA; once you enroll in Medicare, you generally cannot make new HSA contributions.

Original Medicare vs. Medicare Advantage: two different philosophies

Original Medicare is Part A + Part B, run by the federal government. Most people then add either (a) a Medicare Supplement (Medigap) policy plus a separate Part D drug plan, or (b) a Medicare Advantage (Part C) plan sold by a private insurer that wraps Parts A and B (and usually D) into one package with its own network and rules.

Medicare Advantage: private insurers, real tradeoffs—and our view

Medicare Advantage plans are offered by private insurance companies under contract with Medicare. They can advertise low or zero premiums and extra perks, which sounds appealing—especially next to a Medigap premium.

Cons we want pre-retirees to understand before choosing:

· Networks and referrals: Many plans are HMO-style; you may need referrals and pre-authorization for services Original Medicare would not gate the same way.

· Coverage can change every year: Benefits, drug formularies, and provider lists shift during annual enrollment. What worked this year may not next year.

· Harder to return to Medigap: If you later want Original Medicare plus Medigap, you may face medical underwriting outside your one-time guaranteed-issue window—denials or higher rates are possible in many states.

· Incentives misaligned with simplicity: Plans are paid under rules that reward documented diagnoses and utilization management—policy debates continue over whether payments always match real patient need.

On May 21, 2025, CMS announced a major expansion of Risk Adjustment Data Validation (RADV) audits—scaling up reviews of Medicare Advantage contracts (including a push toward annual audits and clearing backlog years). The policy discussion is partly about whether payments to plans align with documented patient conditions. Medicare Advantage is a large, heavily audited private-administered program—not the same thing as Original Medicare.

For many of the families we serve—especially those who value choice of doctors, predictable cost-sharing, and straightforward nationwide access—Original Medicare paired with a Medigap policy and a carefully chosen Part D plan is often the better long-term fit. Medicare Advantage can work in narrow situations, but we rarely see it as the default answer when flexibility and clarity are top priorities.

Standardized Medigap plans: how Part A and Part B work with other plans

Original Medicare has two parts: Part A (hospital insurance) and Part B (medical insurance). They do not cover everything; most people add other coverage.

Part A pays first for covered inpatient hospital stays (after the Part A deductible and any daily coinsurance in a benefit period).

Part B pays first for covered outpatient care—after you meet the Part B deductible, Medicare pays 80% of approved amounts; you owe 20% unless supplemental coverage (e.g., Medigap) applies.

Medigap (if you buy it) works with Original Medicare: it pays its share after Medicare pays what it owes—filling “gaps” like deductibles, copays, and coinsurance, depending on which Medigap plan letter you choose. In most states, Medigap policies are standardized by plan letter—same benefits for a given letter from insurer to insurer; premium is what differs. Plans C and F are not sold to people new to Medicare after January 1, 2020; many newer enrollees compare Plan G and Plan N.

Part D (prescription drug plan) is separate: it does not coordinate line-by-line with Part A/Part B the way Medigap does. You choose a Part D plan for medications; premiums and cost-sharing are on top of Part B (and IRMAA if applicable).

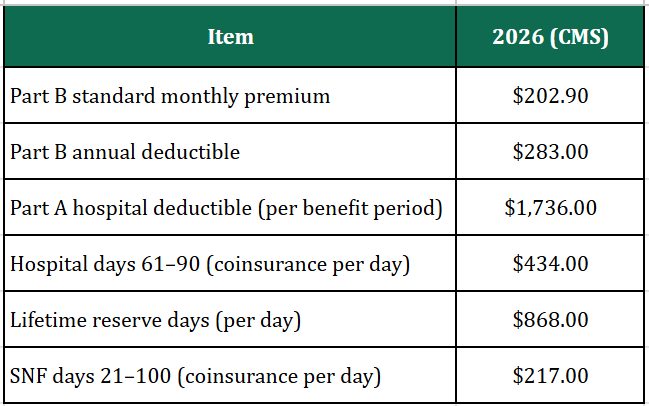

Part A and Part B: key costs (2026)

CMS publishes premiums, deductibles, and coinsurance annually. For 2026, highlights include:

Source: CMS 2026 Medicare Parts A & B Premiums and Deductibles.

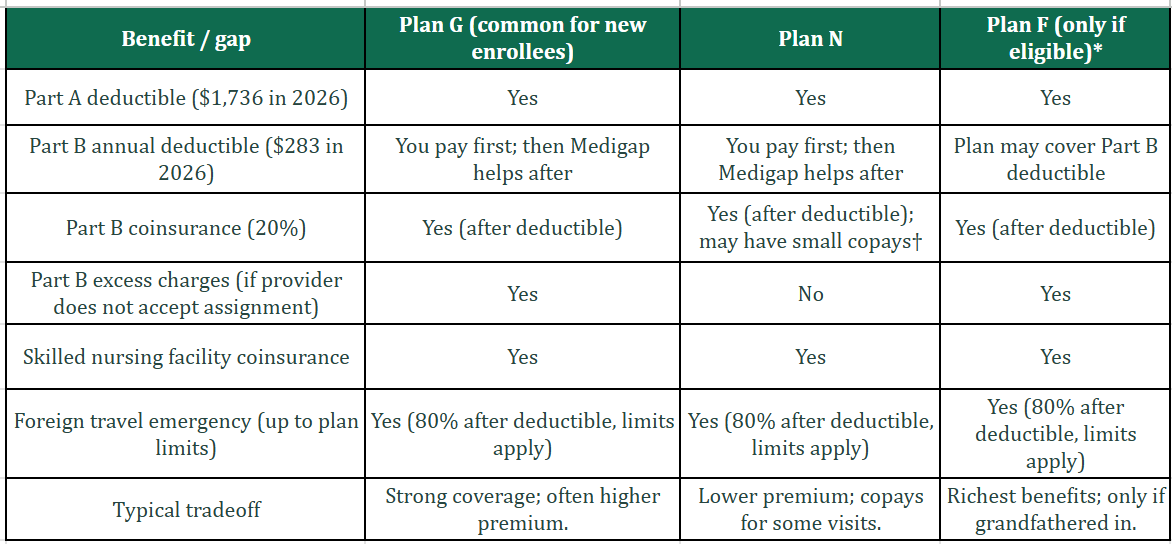

Standardized Medigap plans: what popular letters cover

Below is a simplified snapshot of how a few common plans handle major gaps.

Source: Medicare.gov standardized benefit descriptions. *Plan F (and Plan C) not available to people new to Medicare after Jan. 1, 2020. Plan N may charge up to a $20 copay for some office visits and up to $50 for ER (waived if admitted).

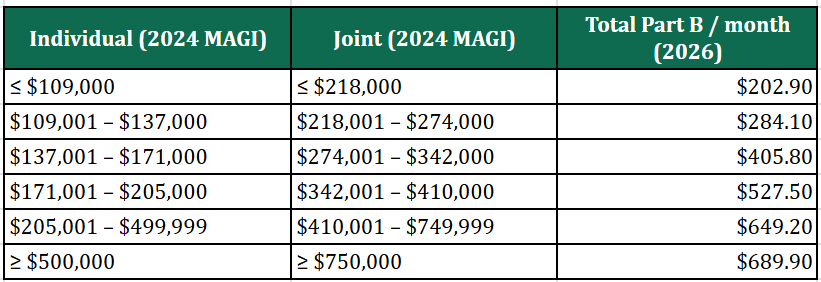

IRMAA: the “two-year lookback” and why retirees overpay at first

Most people pay the standard Part B premium. If your income is above certain thresholds, you also pay Income-Related Monthly Adjustment Amounts (IRMAA) on Part B and Part D.

Here is the part that catches new retirees off guard: IRMAA is usually based on the tax return from two years earlier—not your income the month you retire. For example, premiums you pay in 2026 generally rely on 2024 modified adjusted gross income (MAGI) that the IRS shares with Social Security.

That means your last year of full salary can still drive Medicare surcharges after you have already left work—exactly when cash flow feels tighter.

Appealing IRMAA with Form SSA-44 (with a realistic example)

If Social Security assigned you an IRMAA tier that no longer reflects your life—because you retired, lost income, divorced, lost a spouse, or had another life-changing event—you can ask SSA to reconsider. The tool for that is Form SSA-44 (“Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event”).

You document the event, provide an estimate of your current or expected income, and SSA may use that lower figure instead of the older tax return—if you qualify under their rules.

Example (illustrative, not tax advice):

Marcus files single. On his 2024 tax return, his salary was $165,000, so his 2024 MAGI fell in a bracket that triggers Part B IRMAA for 2026. He retires in March 2025; in 2026 his income is mostly $42,000 from a pension plus taxable Social Security—far lower than his working years.

Without an appeal, SSA might still price 2026 premiums using 2024 data. Marcus gathers his retirement letter, recent pay stubs, and a pension award letter, completes SSA-44, and asks SSA to use a more accurate income estimate. If approved, his monthly Part B (and any Part D IRMAA) can align with his actual retired cash flow—not his peak earning year.

Appeals are not guaranteed; follow SSA instructions and keep copies of everything you submit.

Source: CMS. 2026 Part B total monthly premiums by 2024 MAGI (full Part B).

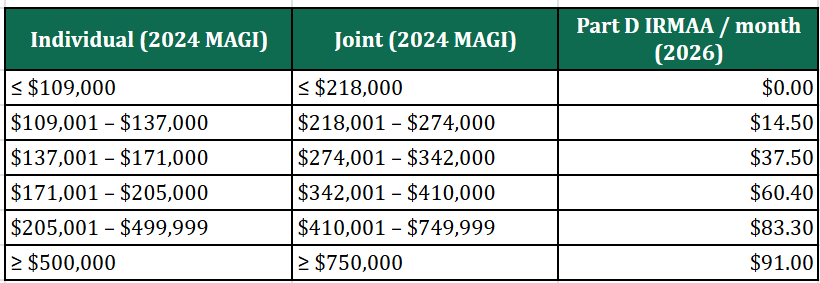

Source: CMS. 2026 Part D IRMAA (added to your Part D premium) by 2024 MAGI. Part D plan premiums are extra and vary by plan and ZIP code.

Do Not Miss Your Medigap “Guaranteed Issue” Window

When Part B starts, you typically get six months to buy a Medigap policy without health underwriting (in most states). After that, insurers may charge more or decline coverage based on health—unless you have a special circumstance. If you think you want Medigap, plan your Part B effective date with that clock in mind.

Part D: shop it like a subscription you renew every year

Drug plans are not “set and forget.” Premiums, deductibles, copays, formularies, and preferred pharmacies change. Re-run the comparison during Fall Open Enrollment (Oct. 15 – Dec. 7).

What to do next

If you are 64 with a pension and Social Security on the horizon, start with three actions:

(1) put your Initial Enrollment Period on the calendar,

(2) model IRMAA using both your last working return and your retired income story—and know when SSA-44 might help,

(3) decide whether you want predictability (Medigap) or are willing to manage network and plan churn (Medicare Advantage).

When you are ready to align investments, withdrawals, and healthcare cash flow, schedule a conversation with US—we help families translate spreadsheets into a retirement you can actually live.

Disclaimer

This article is educational and not individualized insurance, tax, or legal advice. Medicare rules, premiums, and Medigap availability vary by state and change over time. IRMAA uses IRS-defined modified adjusted gross income. For plan selection and appeals, consult a licensed insurance agent in your state and SSA resources; for tax projections, consult a tax professional.