FEHB and Medicare at 64–65: A Straightforward Guide for Federal Retirees

If you’re 64 and counting months until 65, you’re probably juggling FERS, TSP, maybe when to take Social Security—and a growing pile of mail about Medicare. You already have FEHB. The hard part isn’t finding an answer online; it’s knowing what applies to you as a federal annuitant or soon-to-be retiree.

This guide is for that moment: how Part A and Part B work alongside FEHB — not as a replacement, for most people — what your estimated healthcare costs look like with and without Medicare Part B, and what IRMAA means when your income stays in a higher bracket. We walk through average senior healthcare costs and use round-number procedure examples, so you can get a clear sense of what health expenses in retirement actually look like.

Educational only—not enrollment, tax, or medical advice. Confirm everything with your FEHB brochure, OPM, SSA, and Medicare.

Why your federal retiree setup is different

Most people lose employer health insurance when they retire. FEHB is unusual: if you qualify (typically an immediate annuity and five consecutive years in FEHB before retirement), you can keep a group plan, and the government still pays a large share of the premium—by law, roughly 72% of the program-wide weighted average, but not more than 75% of your plan’s premium.

Most FEHB plans bundle medical and prescription in one OPM plan; Open Season lets you switch plans annually; FEHB plans have annual out-of-pocket maximums; many households keep continuity with a carrier they already know. None of that makes FEHB free—it explains why federal retirees often keep FEHB while layering Medicare on top.

So at 65, the question usually isn’t “FEHB or Medicare?” It’s “How do FEHB and Medicare fit together?” and “Do I need Medicare B? And what am I losing if I don’t enroll in Medicare B?”

What typical health spending looks like (the big picture)

Numbers help you breathe. You’re not looking for precision to the dollar—you want a sense of scale: what others in FEHB and Medicare typically pay, so your own choices feel less abstract.

Federal Employees Health Benefits (FEHB) — program scale (OPM, 2026 materials): Roughly 8.2 million people are covered under FEHB/PSHB; across all enrollees (active employees and annuitants), average age is about 60. Premiums move with medical trend—for 2026, OPM reported FEHB average enrollee share up about 12.3% (program average; your plan may differ).

Medicare beneficiaries — out-of-pocket spending: People in traditional Medicare spent $5,460 out of pocket on average for all health costs (premiums + services) in 2016; ages 65–74 averaged $5,021; ages 85+ averaged $10,307 (skewed upward by long-term care for some). “Medical providers and supplies” averaged $712 per person that year across all beneficiaries, including people who used little or no care.

Source for Medicare OOP figures: KFF, How Much Do Medicare Beneficiaries Spend Out of Pocket on Health Care? (MCBS 2016; Nov. 4, 2019).

FEHB + Medicare Part A only vs. FEHB + Medicare Part A and Part B

Start with the roles. For most people, Part A (hospital) is premium-free at 65 if they (or a spouse) have 40 quarters of Medicare-covered work—common for long federal careers.

Part B (outpatient/doctor care) has a monthly premium and a deductible—for 2026, CMS set the standard Part B premium at $202.90/month and the Part B deductible at $283. If modified adjusted gross income is high enough, Part B (and Part D) premiums add income-based surcharges.

With Part A and Part B, Medicare often pays first on Medicare-covered outpatient/professional care (including physician services in the hospital with Part A); FEHB may coordinate as secondary, often waives or reduces certain deductibles/copays.

Without Part B, there is no Part B premium—so you avoid that $2,435/year standard Part B cost at 2026 rates ($3,409/year per person if the couple’s income is over $218,000). But for outpatient care and inpatient professional charges that Part B would cover, Medicare isn’t paying first—your FEHB plan is typically primary for that coverage. Practically, that often means you rely on FEHB cost-sharing (deductibles, copays, coinsurance) for doctor and outpatient services in line with your plan brochure—which can be fine or expensive, depending on use and plan.

So the cost comparison isn’t just premiums—it’s premiums plus how you use care.

FEHB Options People Actually Talk About At Open Season

OPM’s marketplace is broad: for 2026, the Open Season highlights note 47 carriers and 132 FEHB plan options (plus separate PSHB rules for Postal households). Nobody needs every acronym memorized—but it does help to know the families of plans federal employees tend to compare year after year.

The Blue Cross Blue Shield -- Service Benefit Plan family is everywhere in federal benefits conversations. Why people like it: large networks, predictable names, and plan designs many households already understand from years on the job. We'll use this plan as an example in the sections below.

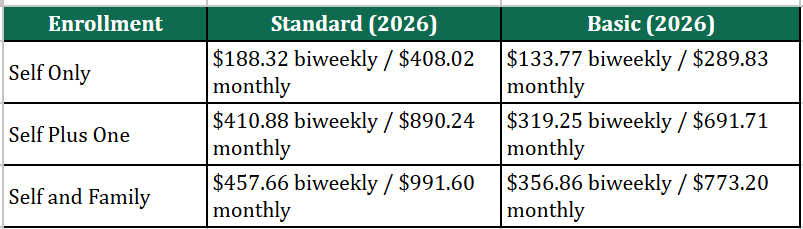

Blue Cross Service Benefit Plan — Basic vs Standard (2026)

Blue Cross Service Benefit Plan Basic vs Standard Premium(2026). Figures from OPM brochure 71-005 (2026), Nationwide rates—opm.gov.

FEHB Outpatient Cost-sharing vs Part B Premium (Blue Cross Example)

OPM does not publish one national average FEHB cost-sharing-only number. Compare your plan’s rules to Part B’s fixed premium.

Illustrative BCBS Service Benefit Plan (Preferred office visits):

Light year—6 PCP + 4 specialist on Basic: 6×$35 + 4×$50 = $410 copays.

Moderate year—8 PCP + 12 specialist on Standard Preferred: 8×$30 + 12×$40 = $720.

Heavy year: imaging, hospital outpatient, or non-Preferred care can add much more.

In a light year FEHB-only copays may be less than the annual Part B premium (~$2,435/year standard, before IRMAA).

Let’s look at the big-ticket care examples in heavy years.

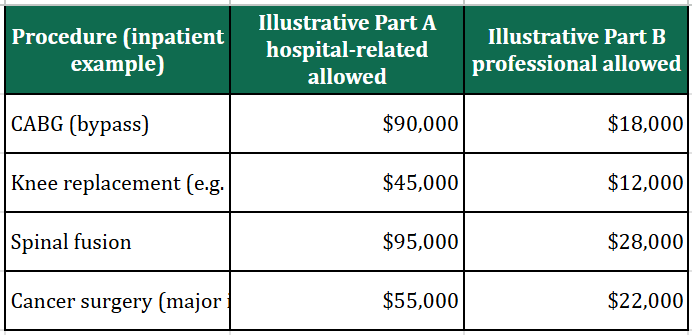

Illustrative Surgery Comparisons: Part A only vs. Part A + B (BCBS Service Benefit Plan, educational only)

We use these four procedures (not a hospital quote) as examples: CABG (bypass), Knee replacement (e.g. TKA), Spinal fusion and Cancer surgery (major inpatient). We show how Part A and Part B amounts split and how FEHB Standard vs Basic and Part A-only vs. A+B change who pays what—intuition for premiums vs. a big one-time bill, not a replacement for your EOB.

Step 1 — How the illustrative bill splits (Part A vs Part B). Round-number Medicare-approved-style amounts:

These are simplified, round-number examples—not predictions of actual claims. They assume Original Medicare, Preferred providers, BCBS Service Benefit Plan (brochure 71-005), one inpatient benefit period, days 1–60, 2026 Medicare: Part A deductible $1,736; Part B deductible $283; Part B coinsurance 20% after Part B deductible on allowed professional charges. Part A only: FEHB professional share uses Standard $350 deductible + 15% of plan allowance after deductible; Basic uses $200 surgeon copay (non-office) + 35% on an illustrative drugs/supplies slice (25% of professional allowance as proxy). Part A + B + FEHB: assumes FEHB wraps Part B patient responsibility so net cash cost is mainly the Part A deductible. Confirm all amounts with Medicare and your carrier.

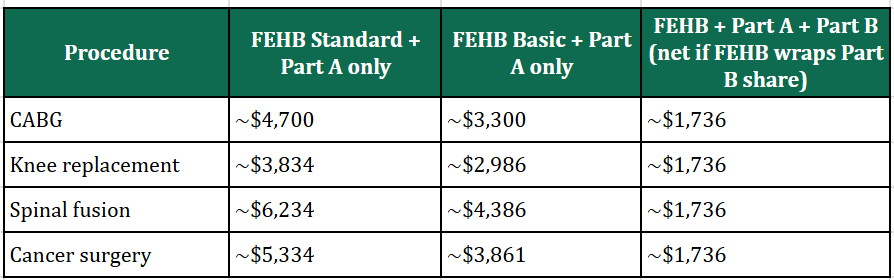

Step 2 — Approximate patient-paid totals (illustrative):

Approximate patient-paid totals for these four procedures (illustrative).

Part A only column: includes the $1,736 Part A inpatient deductible plus estimated FEHB cost-sharing on professional fees when Medicare does not pay Part B benefits.

Part A + B column: mainly the Part A deductible in these examples if secondary FEHB covers Medicare’s remaining patient responsibility on covered services. Outpatient-only procedures, multiple surgeons, non-covered services, or different networks would change results.

So in the heavy years, the out-of-pocket difference between FEHB with and without Medicare Part B is roughly $1,500–$3,500 based on our examples— as the standard Medicare Part B premium of $2,435 per year. These numbers are meant to give you a general sense of the cost comparison. For exact figures, please refer to your FEHB plan's brochure.

Practical checklist

1. Confirm FEHB carry into retirement — five-year rule + immediate annuity eligibility.

2. Calendar your Medicare enrollment window — especially Initial Enrollment around 65 if you’re not on active employer coverage.

3. Model IRMAA — TSP withdrawals, taxable investments, Social Security taxation, and Roth vs. traditional flows all feed the conversation.

4. Shop Open Season every year — plan exits happen; 2026 had discontinued options with defaults announced by OPM.

5. Based on your health and financial situation, weigh both the premiums and the out-of-pocket costs before making a decision.

Bottom line

You don’t need a perfect prediction of health inflation. You need a decision framework: compare FEHB vs. Medicare cost trends honestly, understand Part A-only versus adding Part B in dollars and coordination, pick FEHB options with total cost in mind—not premium alone—and fold IRMAA into retirement income planning if you’re in the higher-income bucket.

If you’re within a few years of 65—reach out for a conversation.

Sources: CMS — 2026 Medicare Parts A & B Premiums and Deductibles (Nov. 14, 2025; includes Part B IRMAA tiers and total monthly premiums); OPM — Federal Benefits Open Season Highlights, 2026 Plan Year (FEHB premium trends; 2025 comparison); KFF — A Snapshot of Sources of Coverage Among Medicare Beneficiaries (employer + Medicare context). Coordination concepts align with OPM — Medicare and your plan brochure.

Disclaimer: This article is general education only and is not legal, tax, medical, or individualized investment advice. Premiums, plan availability, and Medicare rules change. Confirm details with OPM, your FEHB carrier, SSA, Medicare, and your licensed professionals before enrolling or changing coverage.