March Monthly Insight: AI in our daily lives • Investing in a time of war

AI has quietly become part of how I live and work. I use it for financial planning, helping my kids with school, and planning family activities. It’s genuinely useful — but the more I use it, the more I notice two things worth keeping in mind.

First, AI makes it too easy to get an answer. But the real value isn’t always in the answer — it’s in the process of asking and thinking. The most important questions don’t appear all at once; they surface slowly, through writing, re-reading, and pushing back on your own assumptions. When AI hands you an answer instantly, it can quietly skip that whole discovery process. So when I use AI, I try not to jump straight to “What’s the answer?” I start with “What do I actually want to understand?”

Second, knowing whether AI is right is a skill in itself. AI is wrong surprisingly often, and it sounds confident when it is. Cross-check important answers with a second AI. Ask the same question differently. And for anything that really matters — legal, financial, medical — verify with a human professional.

But perhaps the most important thing is this: those of us who are already grown up need to keep learning just like students do — what these tools can do, what they can’t, and how to combine them with human judgment for the best outcome. That learning never really stops.

I’ve come across two items I thought you’d find valuable. Feel free to reach out if you would like to discuss in more detail.

Investment: What the Israel–Iran War Means for Your Portfolio

Last weekend, Israel and Iran went to war. The market reaction was swift: the S&P 500 fell, gold fell, U.S. Treasuries briefly sold off, and international and emerging markets dropped even more. It’s unsettling to watch. So let’s put it in context.

Conflicts can last for years. Markets usually price them in within weeks. Trump has suggested the war could last four weeks, but looking at Iran’s resolve and the region’s history, it could easily run longer. That said, the duration of a conflict and the duration of its market impact are very different things.

LPL Research studied every major geopolitical shock since World War II and found a remarkably consistent pattern:

· Average decline on the day of the event: −1.1%

· Average peak-to-trough drawdown: −4.7%

· Average trading days to market bottom: ~19 trading days

· Average calendar days to full recovery: ~42 calendar days

From outbreak to maximum drawdown, the historical average is less than one month. The Russia–Ukraine war in 2022 is a good example: the S&P 500 actually — counterintuitively — rose 1.9% on the day Russia invaded. Oil peaked around the same time. One year later, the S&P 500 was down only 5.1%, and most of that was driven by the Fed’s aggressive rate hikes, not the war itself.

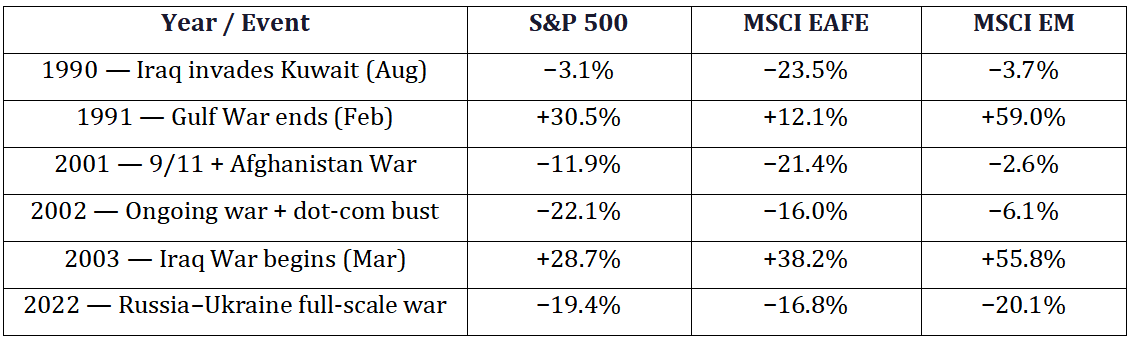

What about international and emerging markets? They are often hit harder initially — but that can also mean they recover faster once geopolitical fear subsides. Here’s how three major indexes have performed in conflict years:

Sources: LPL Research; financialwisdomforum.org (MSCI EAFE); Bloomberg / MSCI (EM). Past performance is not indicative of future results.

A Note on 2022

the MSCI EM index’s poor showing was partly a technical anomaly. MSCI removed Russia from the Emerging Markets index in March 2022, forcing funds to sell Russian stocks at distressed prices. Strip that out, and core EM was highly differentiated: Gulf states (UAE, Kuwait, Saudi Arabia) actually posted positive returns for the full year, while China and Turkey were dragged down by their own domestic issues.

Two things to keep in mind going forward. First, geography matters more than people think: Middle East conflicts tend to hurt European and Japanese markets (large oil importers) more than U.S. markets. Second, emerging markets tend to overshoot on the downside during periods of fear — which means that once uncertainty starts to ease, they can rebound most strongly. I’m watching this closely and happy to discuss how it affects your specific portfolio.

The Value of a Qualified Advisor — and Your Privacy

This one starts with a story. A friend of mine recently got married and reached out to ask if I could refer her to a qualified online will provider. She was willing to pay for the referral. She’s young, newly married, and doing the right things — thinking about the future.

But here’s what gave me pause: she was hesitant to fill out an online form because she didn’t want her personal contact information floating around, triggering unwanted calls and emails. That’s a completely reasonable concern.

She’s not alone in feeling that way. And it’s a good reminder of something I try to offer that online platforms can’t easily replicate: you can come to me, and I will protect your privacy. I will not push products you don’t need. I’ll listen to what you actually want to accomplish and connect you with the right people.

It’s easy to get an answer from AI or an online form. It’s much harder to know if that answer is right for your situation. A will generated by an online service might be technically valid but miss the nuances that matter most to your family. The same is true for insurance quotes, tax advice, and investment decisions. Getting information is easy. Knowing what to do with it, and being confident you’re not missing something important — that’s where a qualified advisor earns their keep.

If you or someone you know has questions about wills, insurance, or just wants a second opinion on a financial decision — I’m here. No forms, no spam, no pressure.

Disclaimer: The content in this material is for general information only and is not intended to provide specific advice or recommendations for any individual. Nothing in this newsletter constitutes personalized investment, legal, or tax advice. Please consult with a qualified professional regarding your specific situation before making any financial decisions.