What Medicare Doesn't Cover in Retirement (2026 Guide)

Most people know Medicare exists. Far fewer know what it actually pays for—and what it leaves behind.

That gap between expectation and reality is one of the most common surprises we see in retirement planning conversations. Healthcare is typically the second-largest expense retirees face. Getting the number wrong can throw off an entire income plan.

The myth: "Medicare will handle it"

Research from the Insured Retirement Institute found that roughly 4 in 10 adults believe Medicare will cover essentially all of their healthcare costs in retirement.

It won't.

A widely cited benchmark from MedPAC analyses suggests Medicare pays roughly two-thirds of expenses for the average fee-for-service beneficiary. The other third—plus long-term care, which Medicare largely does not cover—falls to you.

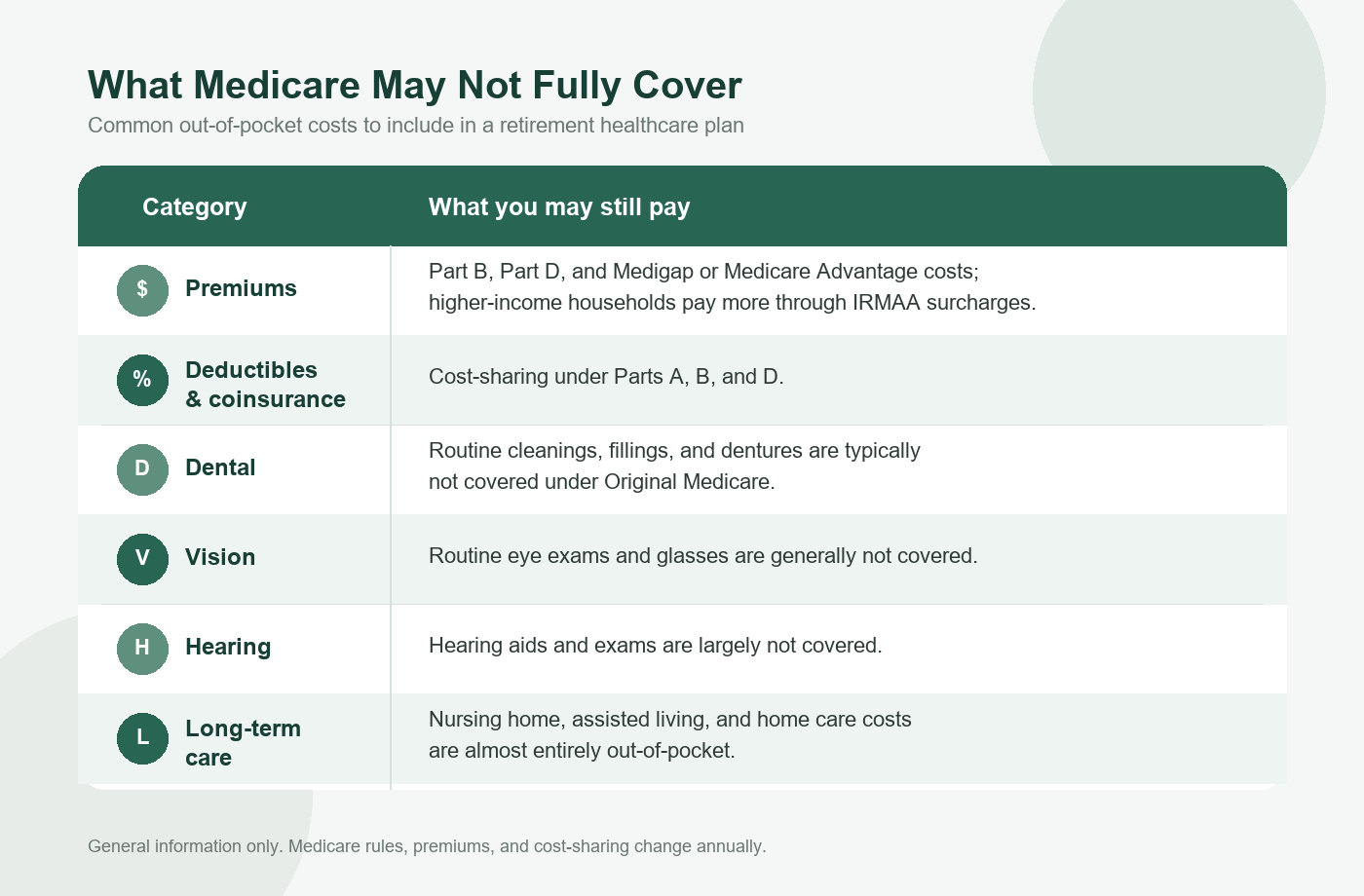

What Medicare typically does not cover

Here is what often shows up as out-of-pocket cost, even with Medicare:

What Medicare May Not Fully Cover

The last category—long-term care—is the one that most often gets lumped in with "healthcare" in people's mental math, even though Medicare does not pay for custodial care. It deserves its own line in your plan. (Long-Term Care Planning: What You Need to Know Before You Need It)

A real number to anchor your thinking

The Employee Benefit Research Institute (EBRI) published an estimate in January 2024 that has become widely used in retirement education:

A healthy 65-year-old couple would need approximately $351,000 (in future dollars) to have a 90% chance of covering projected medical expenses in retirement—not including long-term care.

Use that number as a planning prompt, not a bill. Your actual costs will depend on your health, your Medicare elections, where you live, and how drug costs evolve. If your situation involves expensive prescriptions or chronic conditions, budget higher. If you have employer retiree coverage, your exposure may be lower.

EBRI updates these estimates periodically as Medicare rules and drug benefit parameters change—so revisit the numbers when the rules move.

One more thing: healthcare costs inflate faster than most things

Medical expenses have historically risen roughly 1.5 to 2 times faster than general consumer inflation over long periods (HealthView Services and similar research). That difference compounds over a 20- or 30-year retirement.

The practical implication: do not assume a static cost. Build in an inflation assumption that is meaningfully higher than CPI when stress-testing your plan.

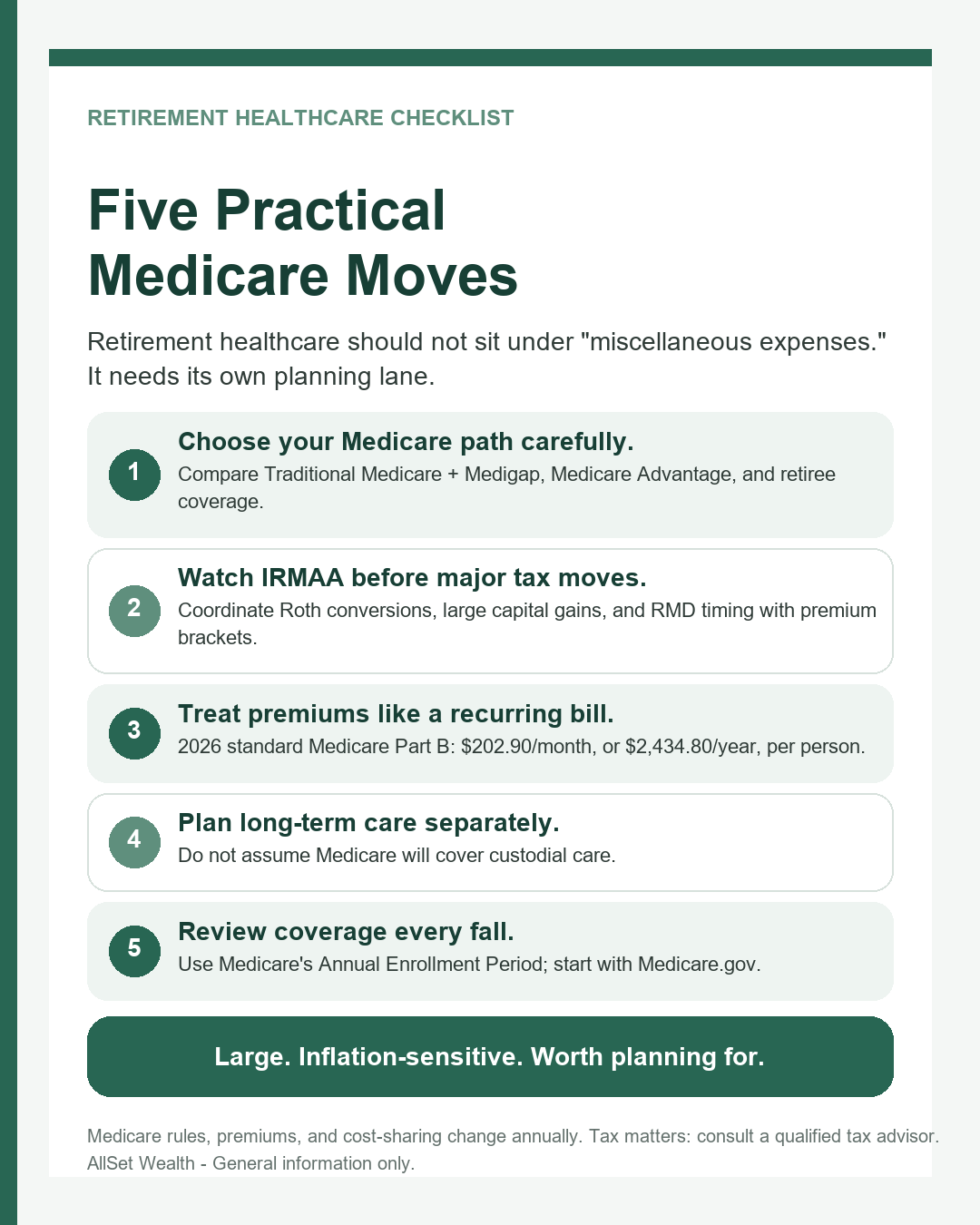

Five moves that actually help

1. Choose your Medicare path carefully.

Traditional Medicare + Medigap, Medicare Advantage, or employer retiree coverage each come with different networks, premiums, and out-of-pocket limits. The right choice depends on your health needs and where you live—and switching later can be difficult.

(FEHB and Medicare at 64–65: A Straightforward Guide for Federal Retirees)

2. Watch IRMAA.

Medicare premiums are income-tested. Higher income means higher Part B and Part D premiums. If you are planning Roth conversions, large capital gains realizations, or RMD timing, coordinate those decisions with your premium brackets—ideally before the two-year lookback that determines your surcharge. (Roth Conversion Gap Years Strategy: Avoid IRMAA & Capital Gains Tax)

3. Treat premiums like a bill, not a surprise.

Medicare Part B alone runs $202.90 per month ($2,434.80 per year) per person at the 2026 standard rate (CMS source; adjusts annually). Build premiums into your monthly withdrawal budget the same way you budget for housing or groceries. (Turning 65? A Smarter Medicare Game Plan)

4. Plan long-term care separately.

Whether you address LTC through insurance, dedicated savings, home equity, family support, or some combination—do not assume Medicare will be the answer. It won't be.

5. Check your plan annually.

Drug formularies change. Coverage gaps shift. Income thresholds for IRMAA are adjusted. Set a reminder each fall during Medicare's Annual Enrollment Period to verify that your coverage still fits your needs. For official program details, start at [Medicare.gov].

Bottom line

Healthcare in retirement is a large, inflation-sensitive liability that requires its own planning lane—not just a footnote under "miscellaneous expenses." The earlier you size the exposure, the more tools you have to address it.

If you want to walk through how healthcare costs fit into your specific income and withdrawal plan, we are happy to help.

Retirement Healthcare Checklist

Disclosures

Securities and investment advisory services offered through LPL Enterprise (LPLE), a Registered Investment Advisor, Member FINRA/SIPC, and an affiliate of LPL Financial. LPLE and LPL Financial are not affiliated with Allset Wealth.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. Medicare rules, premiums, and cost-sharing change annually; consult official program resources and qualified professionals for decisions about your coverage.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.